Curtailing Judicial Discretion – Federal Sentencing (Part Two)

Curtailing Judicial Discretion – Federal Sentencing (Part Two)

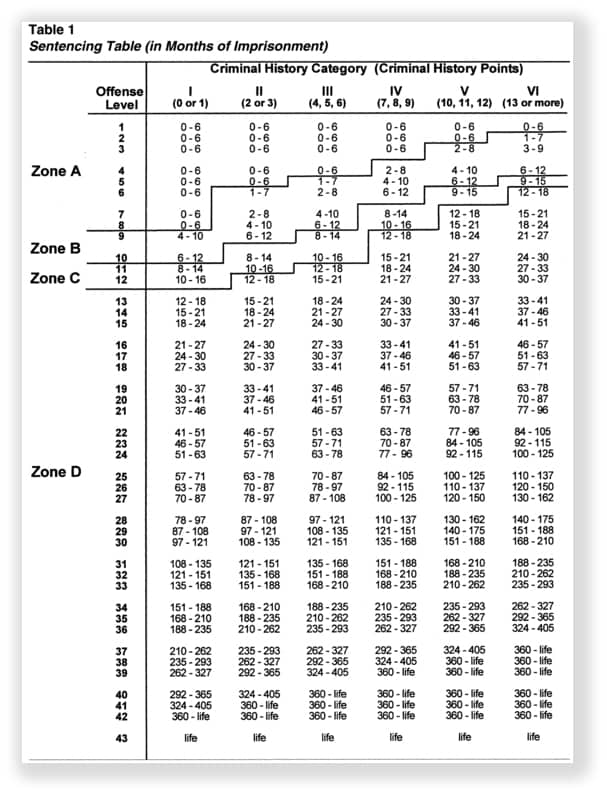

The offense level is only half of the equation for determining the guideline range. The other axis in Table 1 deals with the criminal history of the defendant. Based on the criminal history, the defendant will receive a score ranging from a category I to category VI. There are five ways to obtain criminal history points under the sentencing guidelines:

- Any prior sentence of imprisonment exceeding one year, add three points.

- Any prior sentence of imprisonment of at least sixty days, add two points.

- Any prior sentence not counted in the two above, add one point.

- If the defendant committed the instant offense while on parole, probation, escape status or imprisonment, add two points.

- Any prior sentence resulting from a conviction of a crime of violence that did not receive points under the above, add one point.

The criminal history points are used to determine the criminal history category of the defendant. Across the horizontal axis, the criminal history categories are written in roman numerals. Below the roman numerals are numbers written in parenthesis. These numbers refer to the criminal history points. For example, if a criminal defendant has 6 criminal history points, they will be in criminal history category III.

This category is used alongside the offense level to determine the appropriate guideline range. This is a hotly contested area of litigation. Determining whether a state conviction receives criminal history points at the federal level is complex. Attorneys should read up on all new case law before conceding a prior conviction under the guidelines. In 2018, the Fifth Circuit issued an opinion ruling convictions under the Texas burglary statute are not considered a “crime of violence” for federal sentencing. United States v. Herrold, 883 F.3d 517 (5th Cir. 2018).

Hypothetical Calculation

This is what the recommendation will look like in the real world. If a person is charged with tax fraud under 26 U.S.C. §7206, the criminal tax lawyer will determine the tax loss under USSG §2T4.1. If the tax loss is $1,000,000, the base offense level is 20.

Now let’s assume the defendant’s mitigating and aggravating factors are as follows:

- The defendant pleads guilty early and accepts full responsibility (-3 levels)

- The defendant hid $200,000 offshore as part of the scheme (+2 levels)

- The defendant has one prior felony conviction for theft in Texas where he served a two-year sentence in prison (criminal history category II).

With an offense level of 19 and a criminal history category of II, the defendant is looking at 33-41 months in prison upon conviction.

The guideline range is not the end of sentencing. It is merely a starting point. The district court can go under or over the guideline range based on a variety of factors, including the inadequacy of the criminal history scoring system, statutory minimums and maximums, substantial assistance, and factors under 18 U.S.C. §3553(a).

Mandatory Minimums and Maximums

The mandatory minimums and maximums in a statute further curtail the sentencing latitude of judges in the federal system. The federal penal code will often note a maximum or minimum sentence for certain convictions.

For example, 18 U.S.C. §2252A criminalizes the possession and distribution of child pornography. If a criminal defendant is convicted of possession of child pornography, the maximum sentence is ten years in prison. If convicted of distribution of child pornography, the statute provides for a mandatory minimum of five years and a maximum of twenty years. No matter what the guidelines deem appropriate the sentencing court is mostly restricted to these thresholds.

Substantial Assistance under USSG §5k1.1

One of the most prominent sections for lowering a sentence is found in USSG §5k1.1. Under this section, the government may file a motion with the sentencing court for a reduced sentence if the defendant has provided substantial assistance in the investigation or prosecution of another person who has committed an offense. The sentencing court will look at the usefulness and reliability of the assistance, the nature of the assistance, and the danger to the defendant or his family in determining how far to depart from the recommended guideline range. Most often, the government will recommend a 1/3 reduction in the sentence. However, larger reductions and recommendations of probation are also possible.

The federal government depends on this section to prosecute the highest members of a criminal enterprise. This section pushes low level criminals to “snitch” on the leaders of criminal organizations. Often, it is difficult for the federal government to obtain sufficient evidence to charge leaders who have insulated themselves from criminal liability. The testimony of lower level actors is vital to the success of many major prosecutions.

18 U.S.C. §3553(a) – The Kitchen Sink

In many criminal cases, there will not be a guideline based justification for the district court to depart from the recommended guideline range. This is where §3553(a) becomes an important vehicle for defendants. This section provides the court with additional considerations in determining the appropriate sentence. The district court’s goal in sentencing is to find a sentence sufficient, but not greater than necessary, to meet the requirements of §3553. There are multiple factors listed under §3553(a), but the following three are the most commonly used:

Nature of the Offense and Characteristics of the Defendant (18 U.S.C. §3553(a)(1))

This section will remind defense lawyers of sentencing in state court. State criminal cases are not constrained by the sentencing guidelines, so the main inquiry is the nature of the offense and the characteristics of the defendant.

This section allows the district court to consider any mitigating circumstances which justify going below the guideline range. Every positive characteristic of the defendant should be placed before the district court in hopes of separating the client from other defendants charged with a similar crime. There are certain factors which are relevant in every sentencing. Family history, drug use, community service, country service, existence of dependents, mental health issues, and exceptional acceptance of responsibility are all relevant inquiries under this section.

Other factors will be case dependent. If a person is charged with tax fraud, family hardship and ability to pay back taxes are important considerations. If a person is convicted of possession of child pornography, success in counseling since indictment and expert analysis to diagnose the client’s tendencies can be helpful in assisting the district court in ordering a just sentence.

It is important defense attorneys consider §3553 very early in the representation. Many successful arguments in sentencing exist because defense counsel was proactive throughout the criminal proceedings.

Need for the Sentence Imposed (18 U.S.C. §3553(a)(2))

This section allows the court to look at the justness of the sentence. The court will consider the need for imprisonment to protect the community and the role of deterrence. This section can be used to reiterate the mitigating factors and highlight the reformation of the criminal defendant since charging.

Need to Avoid Unwanted Sentence Disparities (18 U.S.C. §3553(a)(6))

The United States Congress instituted the sentencing guidelines to avoid sentence disparity between similarly situated defendants. The federal system does not want a defendant in Texas getting the maximum on a tax fraud count while defendants in New York receive probation. This core theme allows an attorney to argue for a certain sentence based on other sentences handed down for similar crimes.

The district court will consider the criminal history, offense characteristics, and the criminal defendant’s role in the crime in determining whether other sentences are persuasive reasons for leaving the guideline range. It is important to note sentences for similarly situated defendants both outside and inside the defendant’s current indictment.

Many district courts have departed from the guideline range because another defendant in the same indictment received a lesser sentence. If the two parties have similar roles and similar criminal backgrounds, there is a persuasive argument they should receive the same sentence.

Overview of the Guidelines

The sentencing guidelines have stripped the district courts of most of their discretion in sentencing criminal defendants. The guidelines often dictate how many months a criminal defendant will spend in prison, or if probation is an option. It is important to figure out the sentencing range, and view the §3553 factors, early in any representation. This ensures the client is doing everything they can to minimize punishment if they are convicted of the offense.

The guideline range is determined by finding the base offense level for the particular offense and adjusting for the mitigating and aggravating factors. This final offense level is buttressed with the criminal history of the defendant to determine a range of recommended punishment. This range of punishment will be the center point for all sentencing arguments moving forward.

The sentencing guidelines are very complex. This post in no way covers the intricacies of each guideline factor. But it should give you an overall idea of how federal defendants are sentenced and how large sentences can be levied for white collar crime. A tax scheme which withholds $500 million dollars from the federal government will start at a level 36. That starting point, with no criminal history, is close to 20 years in prison. If you add additional counts, and other aggravating factors, these sentences can become substantial.

The next blog will handle the specific issues with determining tax loss when representing a client for criminal tax violations. The tax loss drives the base offense level in criminal tax cases. It is the single most important sentencing factor. Effectively challenging the government’s tax loss calculations can be the difference between foregoing charges altogether, getting probation, or spending a lengthy time in prison.